| This week, Ambrose Evans-Pritchard writes that central banks need to free themselves from the cult of New-Keynesian economics, and Jeremy Warner has identified six reasons why buyers of the US stock markets might continue to outnumber the sellers. |

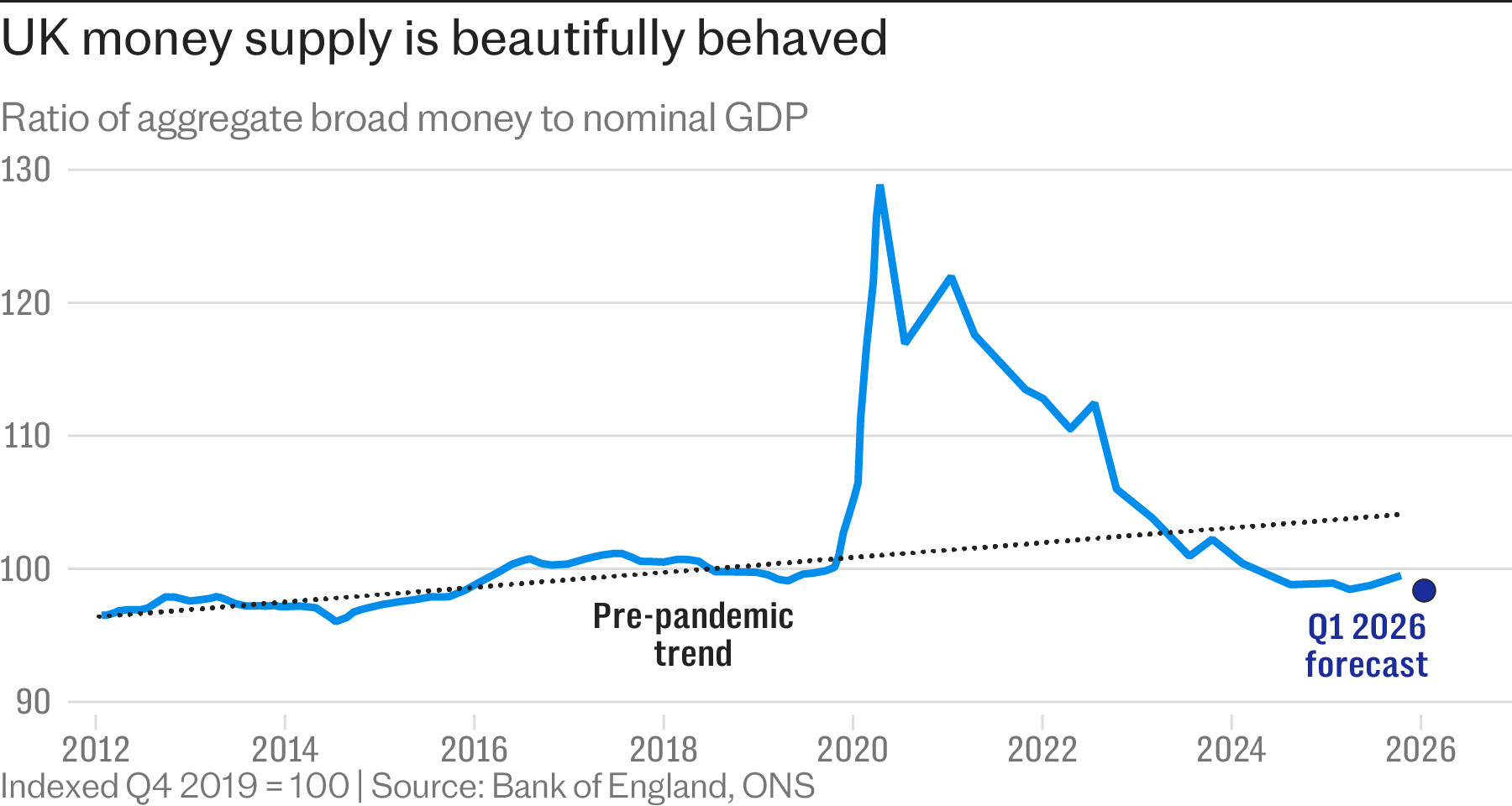

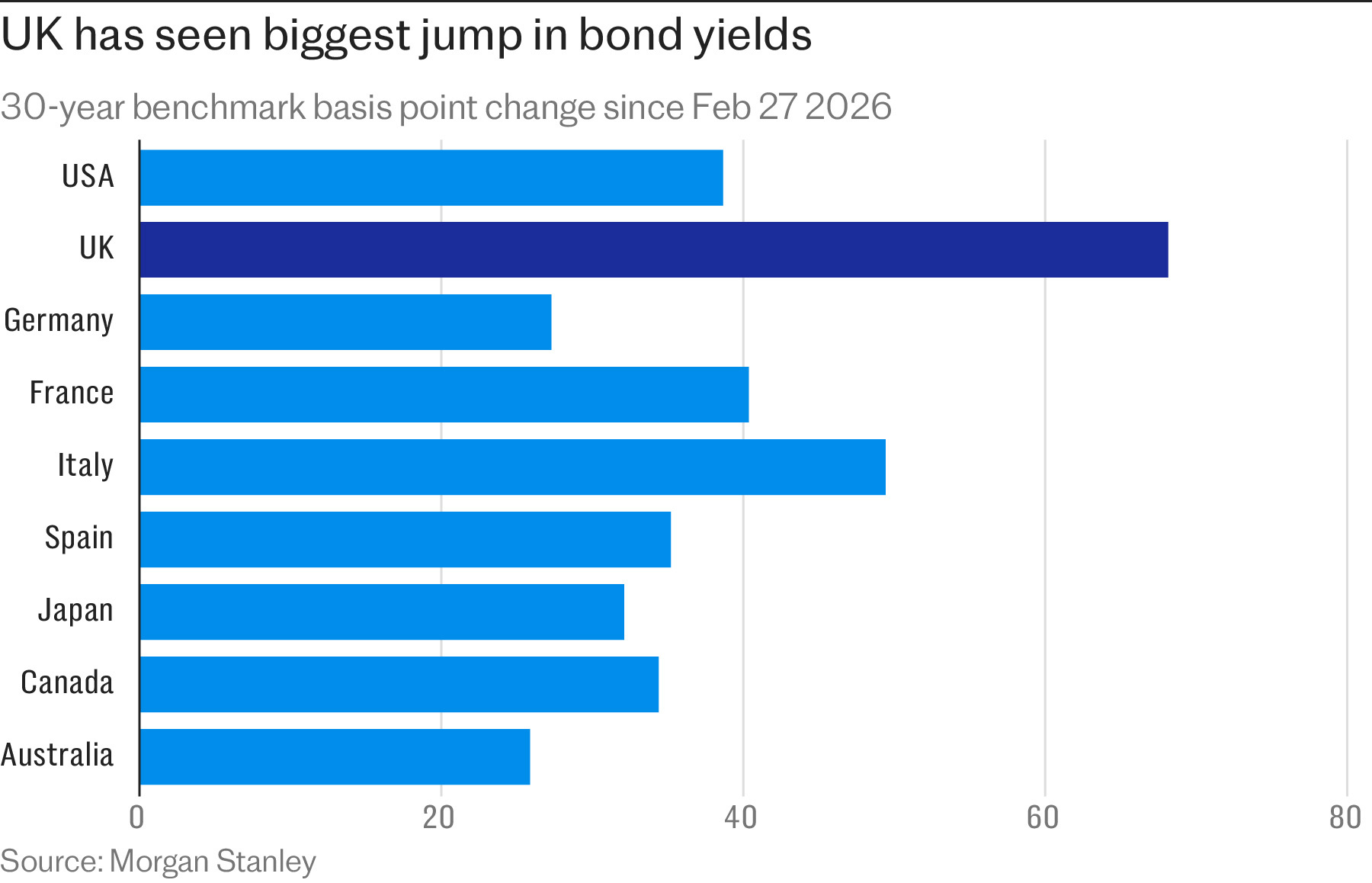

The Bank of England doesn’t have the credibility to challenge the established orthodoxy Credit: Dan Kitwood/2024 Getty Images The Bank of England doesn’t have the credibility to challenge the established orthodoxy Credit: Dan Kitwood/2024 Getty Images Ambrose Evans-PritchardWorld Economy EditorThe US Federal Reserve and the Bank of England are parting ways. The Fed is at last breaking free of a destructive and outdated academic cult. Ambrose Evans-PritchardWorld Economy EditorThe US Federal Reserve and the Bank of England are parting ways. The Fed is at last breaking free of a destructive and outdated academic cult.You could argue – and a few brave heretics dare to whisper such thoughts – that the rational response of central banks to the recessionary shock coming our way from the Gulf is either to keep a steady hand or even to cut interest rates to cushion the blow. But the Bank of England and the European Central Bank (ECB) follow the New-Keynesian lodestar of inflation expectations, the guiding light that has steered Western central banks for decades and shapes thinking at the PhD factories of academia with scant tolerance for dissent. The ECB has made clear that it will raise rates into the teeth of the storm, and a storm there will be because 8pc of world trade is still cut off in the Gulf and Donald Trump still thinks he can prevail with publicity stunts. The Bank of England said it may raise rates six times if oil rises to $120 and stays high for the rest of the year. Are we to assume by reductio ad absurdum that it might raise rates 12 times if crude hits $180? Merely to talk of piling Pelion upon Ossa in this way is to chill investment and kill the housing recovery. This academic model places much weight on “anchoring” public perceptions of future prices. Put crudely, it assumes that if people think inflation is going to be higher, then inflation will be higher and central banks must therefore breathe fire; and if they think inflation is steady, then there is little to worry about and central banks can rest on their laurels. The theory was thoroughly debunked in a paper published by the Federal Reserve board in 2021 entitled “Why Do We Think That Inflation Expectations Matter for Inflation?”. It argues that the central catechism of modern monetary policy “has no compelling theoretical or empirical basis”, relies on “incredible assumptions”, makes predictions that are “wildly at odds” with observable facts, and can lead to “serious policy errors”. Written by senior Fed economist Jeremy Rudd, it starts by declaring that “mainstream economics is replete with ideas that ‘everyone knows’ to be true, but that are actually arrant nonsense”. From there it goes on to twist the knife mercilessly. Economists cling to failing models out of intellectual cowardice but also because “it takes a theory to defeat a theory” and so far the profession has yet to come up with a less implausible one. “It is far, far better and much safer to have a firm anchor in nonsense than to put out on the troubled seas of thought,” says the paper, quoting the economic luminary John Kenneth Galbraith. Rudd says various schools of economics have played their part in this misadventure – including three Nobel laureates, Edmund Phelps, Milton Friedman, and Robert Lucas – but it has worsened over time and culminated in the Lakatosian absurdities of the New-Keynesians, “whose theoretical derivation is even harder to take seriously and whose empirical justification is close to non-existent”. This more or less describes where the Bank of England and the ECB have ended up, though not the post-Powell Fed under the incoming Kevin Warsh, a free-thinker finally willing to declare that the emperor has no clothes.  Kevin Warsh is Donald Trump’s pick to lead the US Federal Reserve Credit: Will Oliver/EPA/ShutterstockInflation expectations gave no forewarning of the Covid inflation spike from 2021-22, for the obvious reason that people “expect” something similar to the recent past. Kevin Warsh is Donald Trump’s pick to lead the US Federal Reserve Credit: Will Oliver/EPA/ShutterstockInflation expectations gave no forewarning of the Covid inflation spike from 2021-22, for the obvious reason that people “expect” something similar to the recent past.The doctrine lulled central banks into a false sense of security. Fixated on this one indicator, they downplayed more meaningful warnings, chiefly surging growth of the money supply, fiscal excess on a wartime scale, raging positive “output gaps” and the tightest labour market for half a century, all stirred together in one great inflationary cauldron. They added fuel to the fire with lashings of quantitative easing. In short, they lost their heads. Warsh was alert to the danger, warning that the Fed was “behind the curve” and risked facing a sudden breakout of inflation. Over the years he has complained that the Fed’s model is broken and that central bankers talk too much, overly reliant on “signalling” and apt to neglect the core truths of fundamental economics. “Inflation is a choice, the result of decisions made by fiscal and monetary authorities,” he said. Inflation expectations led central banks to make the opposite mistake in the summer of 2008 when oil prices reached an all-time high of $147 a barrel ($225 in today’s money). They panicked in the face of rising inflation expectations instead of “looking through” the commodity shock and focusing on the deterioration of the real economy. The ECB raised rates even though much of the eurozone was already in recession: the Fed tightened by talking up the yield curve even though the credit system was disintegrating. It was a pro-cyclical blunder. As they would soon discover, technocrat talk of “second-round effects” was to completely miss the point. Inflation was the least of their worries. The US consumer price index collapsed over the next four months and was falling at an annualised pace of 19pc by that November. The deadly danger would soon be deflation. So what is the danger today in this full-spectrum commodity shock? The rising cost of oil, gas, naphtha, fertilisers, helium, aluminium and other inputs on the wrong side of Hormuz is obviously inflationary for one part of the economy, but is deflationary for the rest of the economy since people have less to spend on everything else. The latter effect may be the more powerful and immediate risk because economic contractions can set off a vicious downward spiral if allowed to metastasise; and the UK and Europe are already at stall speed with rising unemployment. In fairness to the Bank of England, its latest monetary policy report wrestles with the complexities of inflation expectations, fully cognisant that there are wicked trade-offs, torturous time lags, and that sometimes central banks must indeed “look through” inflation shocks. But the point remains: why do they devote so much space and thought to a concept with near-zero predictive power while mostly paying lip service to the money supply, which is anything but inflationary right now.  Nor do I envy the task of Andrew Bailey, the Bank’s Governor. Labour’s refusal to rein in runaway benefits or bite the bullet on taxation has pushed the country to the brink of a gilts crisis, with borrowing costs decoupling dangerously from G7 peers. Nor do I envy the task of Andrew Bailey, the Bank’s Governor. Labour’s refusal to rein in runaway benefits or bite the bullet on taxation has pushed the country to the brink of a gilts crisis, with borrowing costs decoupling dangerously from G7 peers.He now has to manage the fallout from the Gulf just as Labour’s insular and self-indulgent Left hurls the nation into another round of political convulsions. The global bond markets will pounce at the slightest suspicion of fiscal dominance.  Britain’s damaged credibility makes it nigh impossible for the Bank of England to take the lead in confronting New-Keynesian group-think and restoring classical orthodoxies. But the Federal Reserve can, and hopefully will, do the job for the rest of us. Britain’s damaged credibility makes it nigh impossible for the Bank of England to take the lead in confronting New-Keynesian group-think and restoring classical orthodoxies. But the Federal Reserve can, and hopefully will, do the job for the rest of us.Warsh is clearly not going to follow the false lodestar and will not be bounced into performative rate rises by the strident commentariat. His structural view is that AI and China’s gargantuan overcapacity are both powerful deflationary forces for the global economy over time. It is Warsh’s misfortune to be appointed by Trump, who persecuted the outgoing Jerome Powell for refusing to do his bidding and wants a yes-man to prime the economic pump for electoral purposes. The task is made even harder by the fact that Warsh’s billionaire father-in-law is a close Trump confederate and an instigator of the Greenland escapade. But let us not visit the sins of the syndicate on the talented beau-fils. Warsh has another insight that is highly relevant to today’s dilemma: shocks caused by wars and supply chains may cause a violent one-off jump in the price level, but that is not remotely the same thing as inflation. He says central bankers should ask themselves “what really is inflation?” before shooting from the hip and lurching in one wrong direction or another. The New-Keynesian priesthood has met its nemesis. |

Public service announcement READ!!!!!!!!!!!

https://www.wired.com/story/a-device-hidden-in-cars-across-the-us-leaves-them-vulnerable-to-hacking-and-paralysis-patch-...